Psychology in financial markets is a complicated matter. History has given us numerous examples of periods when irrational thinking drove markets to obscene highs before they came crashing down following a defining moment.

This phenomenon is called a ‘bubble’, a term used because price movements mirror the life cycle of a soap bubble – euphorically expanding and, inevitably, bursting.

Markets are intended to reflect the collective wisdom of millions of participants who price assets.

This wisdom is based on:

- Supply and demand – enabling price discovery;

- The liquidity of assets – allowing them to be traded easily without significant moves in the price; and

- Market efficiency – allowing assets reprice swiftly upon the introduction of new information.

Over centuries, we have witnessed several episodes of market mania, whereby prices completely detached themselves from the underlying value of an asset. In fact, these bubbles are among the most studied events in economic history, yet, somehow, they continue to recur.

What makes bubbles so fascinating isn’t just the spectacular rise and looming collapse, but also the remarkable consistency of the psychology that drives them.

From 17th Century Amsterdam to 21st Century New York, the same patterns emerge: an innovation excites the market, prices rise rapidly, and a relentless greed for success takes hold.

Each time, we find market participants creating valuation justifications under the guise that ‘This time it’s different’.

History has proven otherwise, as evidenced time and time again.

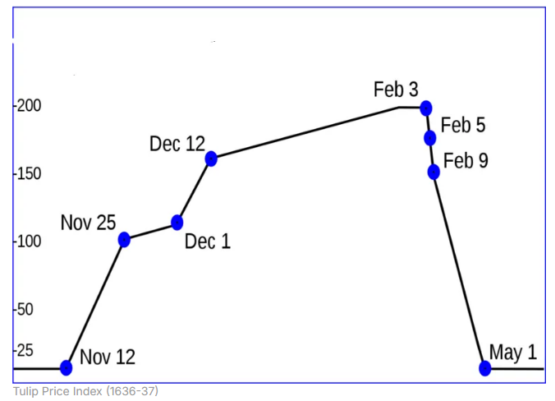

Tulip mania

Going all the way back to 1636 in the Netherlands, a virus caused tulip bulbs (yes, the flower) to display lively new colours and patterns. The phenomenon created a buzz among wealthy merchants and sparked enormous speculation in the tulip bulb market.

Tulips were seen as more than just flowers; they became symbols of status and wealth, having already been regarded as exotic imports from the Ottoman Empire. The excitement was so rife that it drove up the price to be in the ballpark of a house in Amsterdam.

Trade was largely facilitated through futures contracts that changed hands rapidly, while the physical tulip bulbs remained buried in their fields.

The psychology that unfolded felt rational. Collectively, investors convinced themselves that the scarcity of the asset created lasting value. With exclusivity and constrained supply, rising prices seemed inevitable. Buyers did not see speculation; they believed they were buying a permanently scarce asset in a growing market of affluent demand.

The mania ended abruptly when an auction for such tulips went unattended, driven by a sudden market consensus that the gains were unsustainable.

Source: Corporate Finance Institute

Above is a visual representation of the price action during Tulip Mania, referring to the Tulip Price Index.

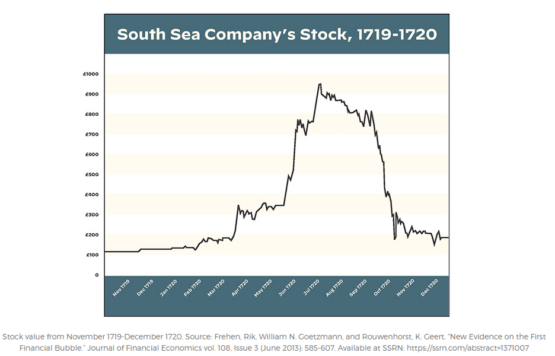

The South Sea bubble

More than a century later, the world witnessed the same phenomenon all over again – this time in 1720 London, when a company with parliamentary backing conducted what is widely regarded as the world’s first Ponzi scheme.

The South Sea Company had been formed as a public-private partnership designed to help manage Britain’s national debt in exchange for monopoly trade rights in the Spanish-controlled Americas.

Excitement around the company surged as the British expected to achieve similar success in the Americas’ slave trade as they already had with the East India Company. The reality was that the entire scheme was destined for failure, given the British Empire had no control over the region.

The Spanish restricted access, rendering the South Sea Company unable to generate any real profit. But back in London, the illusion of prosperity persisted, with the company issuing new shares and swapping them for more government debt.

The share price soared from £120 to almost £1 000 in just a few short months. When confidence finally faltered later that year, the share price collapsed back to £120, wiping out the fortunes of many – including Sir Isaac Newton, who is estimated to have lost the equivalent of £4 million in today’s money.

A longer backstory, but a remarkably similar psychology. A company with parliamentary backing, the endorsement of the king, and monopoly trade rights in a market that had already proven successful led investors to believe that risk had been eliminated and profits were assured.

Once again, the market rationalised these events and convinced itself that this was not speculation at all.

Source: Journal of Financial Economics

The dot-com bubble

Fast forward a couple of centuries to a world we recognise today.

Approximately 12 years after the birth of the internet, the web had become commercially accessible, and e-commerce businesses emerged as the latest craze to engulf the markets.

Startups with little more than a domain name and lofty ambitions were eagerly moving for a listing on the Nasdaq, and investors were willing to fund these fantasies.

In the same fashion as the South Sea Company, most of these businesses were rapidly burning through the cash they raised to finance expansion.

The reality of the dot-com bubble was that most of these companies had no real path to generating free cash flow.

Traditional valuation metrics such as price-to-earnings (PE) ratios were dismissed as outdated given the revolutionary nature of the internet.

Analysts began inventing metrics including “price to clicks” and “price to eyeballs” to justify the sky-high valuations.

The ease of funding in the US enabled the mania to continue for almost five years until, inevitably, capital began to dry up and the confidence that fuelled the move soon evaporated.

A vastly different era, but once again, the psychology remained the same.

Without a doubt, the internet has proven to be the greatest revolution of modern history, fundamentally transforming media, communication and commerce all together.

The rush to get involved in this revolution early, on the premise that it would guarantee long-term wealth, was a flawed thought. The technology itself and the adoption of e-commerce were very real, as demonstrated by the success of Amazon, but the belief that each and every single e-commerce company would be a massive success story proved to be yet another critical error in investor judgement. Just ask anyone who invested in Pets.com.

Subprime mortgages and the global financial crisis

The most well-documented of all, the global financial crisis, was the outcome of reckless lending and exotic derivative instruments that overly inflated the US housing market, under the premise that prices could only ever rise.

US banks created and sold highly complicated mortgage products to consumers who were unable to afford the repayments. They went on to package these low-quality financial assets into mortgage-backed securities and collateralised debt obligations and proceeded to sell these products to investors around the world as AAA credit instruments, under the pretext that the risk had been effectively diversified.

To the broader public, faith in the US housing market appeared rock solid, and this message was well broadcasted with institutional and federal support.

As we saw from tulip bulbs to internet companies, in 2007, house prices across the US began to decline, while borrowers were already defaulting on mortgage payments. This marked the onset of the looming collapse in the US housing market.

The belief that the system simply could not fail was once again deeply flawed.

This time around, investors of all tiers were affected, with major banks such as Lehman Brothers filing for bankruptcy and millions of families losing their homes to foreclosure.

Source: Author-provided

Having explored centuries of bubbles, the pattern becomes remarkably clear.

This brings us to 2026. Is artificial intelligence (AI) the latest bubble?

Speculative headlines suggest it might be, but the health of the major AI players tells a different story.

Big tech stocks such as Nvidia, Alphabet and Meta have all seen rapid upward moves in their share prices. As of late, scepticism has begun to creep into the sector, as the market ponders the very same question.

Where the pattern recognition falls apart in the case of big tech lies in the real earnings of these conglomerates.

The latest earnings display incredibly strong fundamentals and structural demand, rather than speculative justification:

- Nvidia reported $57?billion in revenue in the third quarter of?2025 alone, with almost 90% coming from data-centre AI chips.

- Alphabet’s revenue for the fourth quarter of 2025 reached $113.8?billion, an 18% year-on-year increase, primarily driven by a remarkable 48% growth in Google Cloud.

- Meta Platforms posted $59.9?billion in revenue for the same period, a 24% year-on-year rise, underpinned by robust advertising growth and AI?powered ad tools.

- Amazon generated an incredible $213.4?billion in revenue for the period, an increase of 13.6% year-on-year, with Amazon Web Services alone contributing 17% to this figure.

These are incredibly strong revenue numbers, even as the companies aggressively forecast further capital expenditure to fuel future growth.

For these companies, margins remain strong, and healthy free cash flows continue to be generated.

This is no longer ‘price to clicks’. It is now about institutions with well-established moats, rock-solid balance sheets and significant intellectual property advantages over their competitors.

Where one still gets a sense of vertigo is in the assessment of valuations.

Using FactSet data, Nvidia is still trading at a premium of 41x forward earnings while peers such as Amazon and Meta trade at a more attractive 26x and 22x forward PE respectively – a discount relative to the broader S&P 500 which currently trades on a forward PE of 28x.

Very importantly, the entire AI market cannot be painted with the same brush. Certain corners look much more concerning and exhibit quite distinct characteristics from big tech.

Take Palantir Technologies, an AI software company that has been the darling of many speculative traders – it trades at an eye-watering forward PE of 102x. That is a play on perfection, and if Palantir were to disappoint in growth expectations, investors would be sure to feel the impact.

Palantir is not alone in this phenomenon: numerous smaller companies within the AI theme display similar traits, often while remaining deeply loss-making. Once again, the narratives used to justify these valuations have a similar ring to prior bubbles …

This time it’s different …

The reality is that it might just be. Maybe this time they are correct.

To reiterate, psychology in financial markets is a complicated matter. The same greed that fuelled all previous bubbles still exists – maybe now more than ever.

Markets can be both rational and irrational at the same time, so it is imperative to position oneself accordingly.

The answer to the question is yes and no. Big tech has the earnings, balance sheets and the power to substantiate lofty valuations, but the more speculative fringe of the AI market includes loss-making stocks trading at indigestible valuations.

AI is being heralded as the greatest technological advancement since the internet, with the potential to transform industries and change lives. History tells us that incredible innovations have come before, and markets have been similarly excited.

In the rush of it all, it helps to reflect on hard-earned lessons of the past. Not all companies will be winners in the theme and fundamentals still matter. That’s a pattern history teaches us we can rely upon.

Uvaal Singh is a portfolio manager at Sasfin Wealth.

Moneyweb does not endorse any product or services being advertised in sponsored article on our platform.

#History #Market #Bubbles #Question